- Media and entertainment sectors expecting an average EBITDA margin of 28%, outperforming leading cross-industry market indices

- EBITDA margins for media and entertainment companies increased each year since 2011 and are expected to remain constant in 2015

- Digital media adoption and expansion into emerging markets is driving profitability

The media and entertainment (M&E) industry is expected to generate higher margins than several leading stock market indices, according to an EY report. Spotlight on profitable growth: Media & Entertainment Vol. VIII provides a performance comparison of the overall M&E business to major stock market indices as well as a ranking of 11 M&E industry sectors on both their profitability and profitability growth rate.

M&E industry earnings before interest, taxes, depreciation and amortization (EBITDA) have increased every year during the period 2011 to 2014 and are expected to remain constant in 2015 as companies continue to leverage digital media, deliver new consumer experiences and expand into emerging markets.

John Nendick, EY’s Global Media & Entertainment Leader, says: “The evolution of the M&E industry continues to focus on the exploitation of digital distribution and finding new and innovative ways to reach and interact with the consumer. With surging demand for content, M&E companies are growing their profitability through multiple consumer offerings, better knowledge of consumer tastes and preferences and continued international expansion.”

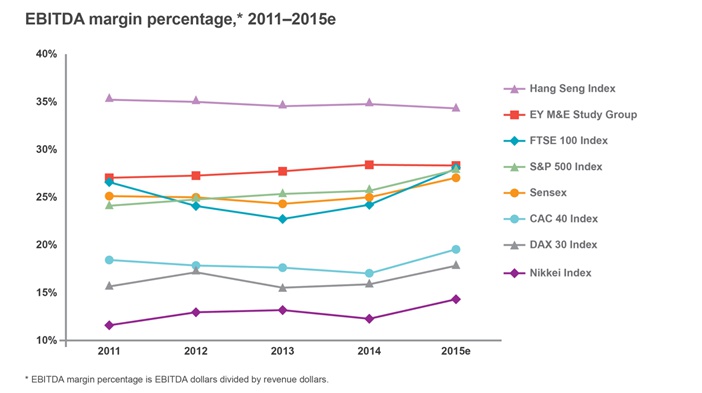

In 2015, it is estimated the M&E industry will outperform several major cross-industry stock market indices (Figure 1). The 11 sectors of the M&E industry measured by EY are expected to have a 2015 estimated profit margin of 28.3%, second only to the Hang Seng Index, 34.3%; followed by the FTSE Index, 27.9%; the S&P 500 Index, 27.8%; the Sensex, 27.0%; the CAC 40 Index, 19.5%; the DAX 30 Index, 17.9%; and the Nikkei Index, 14.4%.

Looking at the 2011-2015e compound annual growth rate in terms of EBITDA dollars, the M&E industry is the third fastest-growing industry as compared to leading stock market indices at 7%, behind the S&P 500 Index at 10% and the Hang Seng Index at 8%; and ahead of the FTSE 100 Index, 6%; the DAX 30 Index, 4%; the Nikkei Index, 4%; the Sensex, 3%; and the CAC 40 Index, 0%.

Figure 1:

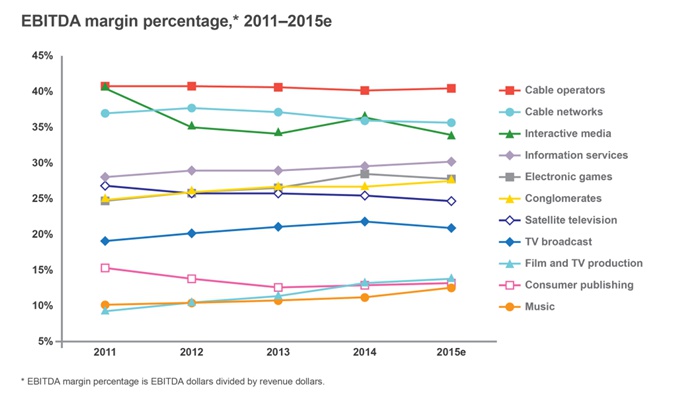

When looking at the estimated 2015 profitability of the 11 M&E sectors (Figure 2), cable operators are expected to have the highest profitability at 40%, followed by cable networks, 36%; interactive media, 34%; information services, 30%; electronic games, 28%; conglomerates, 28%; satellite television, 25%; TV broadcast, 21%; film and TV production, 14%; consumer publishing, 13%; and music, 13%.

A review of the 2011-2015e compound annual growth rate in terms of EBITDA dollars indicates that interactive media is the fastest growing media and entertainment sector at 17%, followed by film and TV production, 14%; music, 9%; electronic games, 7%; conglomerates, 6%; cable networks, 6%; TV broadcast, 5%; information services, 4%; cable operators, 4%; satellite television, 4%. Only consumer publishing is projecting a decline, estimated at 7%.

Figure 2:

Highlights across the 11 M&E sectors include:

- Cable operator margins continue to be the highest among all M&E sectors as a result of high-margin data and business-to-business services. Margins remain stable due to price increases despite rising programming costs and increasing competition from over-the-top (OTT) services.

- Cable networks are benefiting from digital licensing, affiliate fee increases and international expansion. However, profit margins are partially offset by rising programming costs and declining viewership on linear television platforms (mainly due to cord cutting or cord shaving). Additionally, advertising revenues have been under pressure, further impacting EBITDA.

- The interactive media sector is growing from mobile monetization, targeted product launches for emerging markets and continued growth in online video and programmatic advertising — resulting in the highest compound annual growth rate (CAGR) among all M&E sectors.

- Information services companies are reporting stable revenues and margins as they increase focus on digital subscriptions and transition from information reference tools to data analytics and visualization-based decision tools to grow EBITDA dollars.

- Growth in the electronic gaming sector is coming from an increase in mobile gamers and the implementation of multiple monetization models such as subscriptions, micro transactions, accessory sales and downloadable content. Continued engagement of console gamers and focus on core franchises will drive EBITDA dollar growth.

- Premium content and increased scale through international and digital expansion are benefiting conglomerates. A focus on profitable assets such as cable networks is further driving growth. However, pressure on advertising revenues is impacting EBITDA for those conglomerates that have segments relying on this revenue source.

- Amid rising content costs, muted subscriber growth and increasing competition from over-the-top services, satellite television companies are consolidating to derive cost synergies and drive profitability.

- Television broadcasters are benefiting from industry consolidation in the US, increases in retransmission fees and growth in digital distribution and international syndication. Similar to other sectors, revenue growth may slow as a result of flatter advertising sales.

- The growth in film and television production is spurred by rising international theatrical revenues, a growing high-margin TV production business and increasing revenue from digital and international licensing.

- Consumer publishing companies continue to face structural declines in print. Digital advertising and subscriptions contribute a relatively smaller percentage to EBITDA dollars and are yet to yield significant returns.

- Digital streaming services and music publishing continue to drive growth for music companies. The sector’s EBITDA margins are gradually rising, from 10% in 2011 to an estimated 13% in 2015.