- DNA of Real Estate report tracks European office, retail and logistics sectors with growth most noticeable in CEE and Semi-core markets, notably retail and logistics.

- Widespread rental growth in European office market reaches six-year high of 0.8% in first quarter of the year.

- Modest yield compression as yields stand at record lows in many markets

Rental growth in the European office market reached its highest point since the beginning of 2012 in the first quarter of the year, according to Cushman & Wakefield’s latest DNA of Real Estate report.

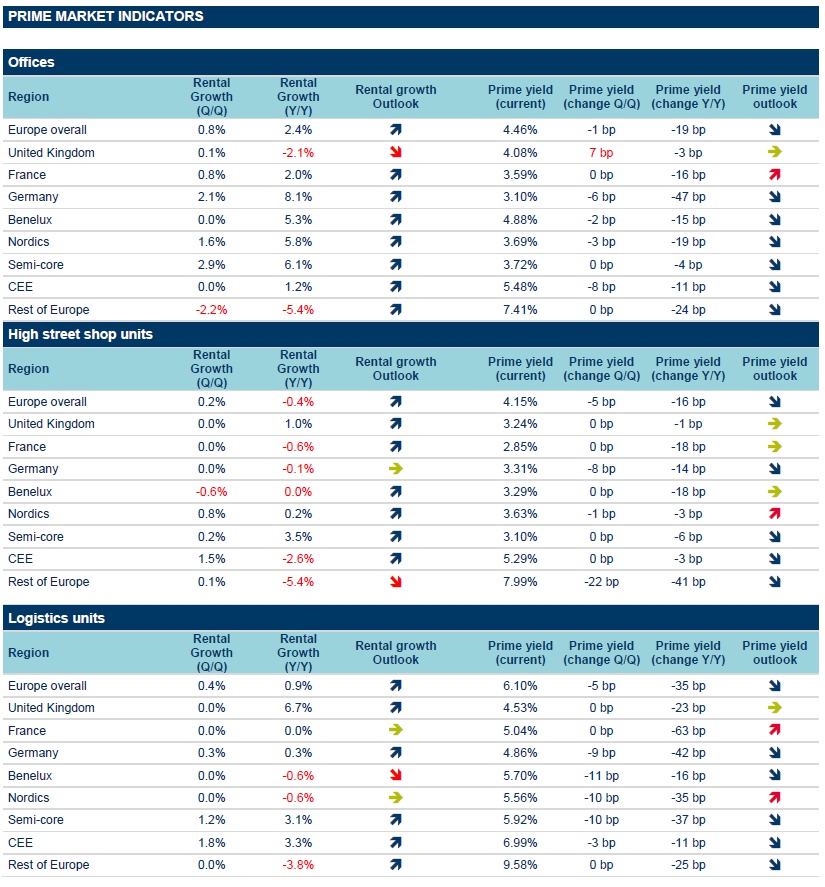

The sector’s strong rental growth is supported by continued positive performance across German, Nordic and Semi-core markets*, which pushed weighted growth across Europe to 0.8% quarter-on-quarter (q/q). This was more than the logistics sector (0.4% q/q) and high street retail which returned to growth with a modest 0.2% q/q.

Yield movements have been more modest in the first quarter with both retail high street and logistics moving in 5bps to 4.15% and 6.1% respectively. Office yields edged in a modest 1bp to 4.46%. The means European prime weighted yield for both offices and logistics are now at their lowest on record.

Offices

Office rents grew by 0.8% in Europe, the highest quarterly growth rate in the past six years. The last four quarters have seen positive growth in at least 15 out of the 47 monitored office markets, providing clear signs of positive momentum in leasing markets. Growth this quarter was led by Milan at 5.6% q/q supported by strong demand, especially in central locations. Prime rents in Berlin grew by 5.2% q/q and by 16.2% y/y while both Dusseldorf (3.7%) and Munich (1.4%) also registered continued rental growth.

Nigel Almond, Cushman & Wakefield’s Head of Data Analytics, said: “We continue to see solid growth in the German office leasing market, supported by strong demand and low vacancy rates. Berlin has one of the lowest vacancy rates globally, at 2.2%, which has driven up prime rents in the city. This has also been the case in other key German cities with further growth expected over the course of 2018.”

Following six quarters of falling rents, the UK registered a modest 0.1% q/q growth at a national level, although with rents on an annual basis still negative it is evident that a lack of clear direction on Brexit talks is delaying investment and occupier decisions.

Overall office yield was down 1bp in Q1 with many markets in the late phase of their cycle as prime yields hit record lows in many markets. Pockets of movement are still evident.

UK regional markets stand out in this quarter with 25bps inward movements recorded in Cardiff, Bristol and Glasgow, and 50bps recorded in Edinburgh. However, this was offset by the 25bps outward movement in London’s West End, with the weighted UK prime yield 7bps higher at 4.08%. Further compression has been evident across Germany (down 6bps to 3.1%) supported by strong leasing markets, with yields across CEE 8bps lower at 5.48%.

Logistics

Rents were flat in the majority (39 out of the 45 monitored) logistics markets in the first quarter of 2018. Overall European rents grew 0.4% q/q. Growth was mostly limited to a handful of locations in CEE (+1.8%) and Semi-core (+1.2%), with a more modest 0.3% rise in Germany. Notably, Lisbon posed a 7.1% quarterly growth in Q1 due to strong demand, driven by e-commerce, and very limited supply of high-quality logistics space. Rents in Warsaw, which benefit strong demand from logistics and e-commerce operators, grew 2.9% q/q.

Lisa Graham, Head of Logistics and Industrial Research & Insight, Cushman & Wakefield, added: “Although rents have been flat for larger logistics facilities, there is growing demand and competition for smaller urban logistics solutions on the edge of cities. As operators streamline their supply chains it is driving higher rents for these smaller facilities, which is set to continue over the long term.”

Logistics yields fell in a third of the monitored markets, with the weighted prime European yield 5bps lower at 6.1% – a new historical low. More than two thirds of markets saw yield compression over the past 12 months, with France (-63bps) outperforming all other regions. Yields in almost all major logistics markets in Europe are now at their 10-year low, although the gap relative to other sectors is still above levels seen in the previous cycle.

High Street Retail

Having posted negative growth over the past two quarters, high street retail rents across Europe grew by a modest 0.2% over the quarter. Rental growth remains patchy with only 8 out of the 45 monitored markets posting growth. These were mostly in CEE and led by Budapest (8.3%) where a stronger economy, growth in wages and household consumption, and rising demand from retailers is pushing rents higher in the main shopping street. Similar fundamentals supported rental growth in Sofia (4.2%) and Prague (2.3%).

High street retail yields compressed by a further 5bps in Q1, and a total of 16bps in the past 12 months, to reach a 10-year low of 4.15%. Markets in France, Germany and Benelux where current yields are among the lowest in Europe contributed most to this compression, reflecting the enduring interest in retail properties in these regions from both domestic and international investors. Yield movements in the UK, CEE, Nordic and Semi-core markets are minimal year-to-date and are not expected to fall much by the end of this year.