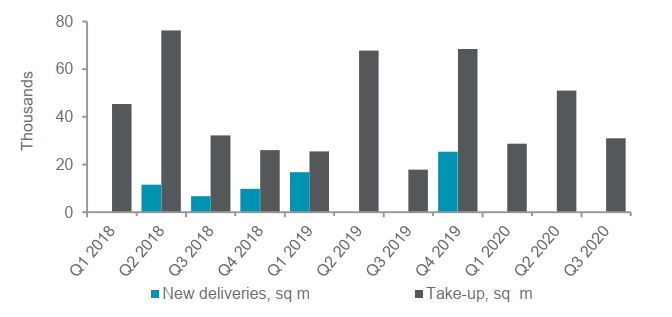

Take-up in the warehousing and logistics property sector in the Greater Kyiv area reached around 31,000 sq. m in Q3 2020, which was around 75% more than the figure for Q3 2019. Development of e-commerce and grocery retail ensures the stable demand in the warehousing and logistics property market. In Q1-Q3 2020, there were no new deliveries on the warehousing and logistics property market in the Greater Kyiv area, however, around 103,000 sq. m of new warehousing space still may be commissioned in Q4 2020 with additional 60,000 sq. m in pipeline for 2021.

Demand

Take-up in the warehousing and logistics property sector in the Greater Kyiv area reached around 31,000 sq. m in Q3 2020, which was around 75% more than the figure for Q3 2019 and similar to Q3 2018.

Take-up for Q1-Q3 2020 amounted to around 110,800 sq. m, which is similar to the figure in the respective period of 2019, but 30% less than the figure for the first 9 months of 2018.

Cushman & Wakefield estimates that net absorption in the sector amounted to around 8,620 sq. m in Q3 2020, which is similar to Q2. Though in March 2020 several lease transactions were postponed till after the quarantine, and in Q1 2020 net absorption was negative, occupier dynamics in the Greater Kyiv area remained generally stable during the most of Q1-Q3 2020.

Key warehousing lease transactions, Q3 2020

|

Property |

Location |

Tenant |

Tenant sector |

Area, sq. m |

|

BF Terminal (phase 2) |

M-06, E40 |

Rozetka |

E-commerce |

14,000 |

|

BF Terminal (phase 1) |

M-06, E40 |

Allo |

Retail |

6,000 |

Source: Cushman & Wakefield

New Supply

In Q1-Q3 2020, there were no new deliveries on the warehousing and logistics property market in the Greater Kyiv area. Nevertheless, in view of stable low vacancy that decreased to record low levels towards the end of 2019 and the prospects of the sector in light of COVID-19, development activity picked up. As of October 2020, Cushman & Wakefield projects that around 103,000 sq. m of new warehousing space still may be commissioned in Q4 2020 with additional 60,000 sq. m in pipeline for 2021.

Warehousing space take-up and new delivery

Source: Cushman & Wakefield

Vacancy

Primary vacancy in the logistics and warehousing property sector in the Greater Kyiv area reached 2.2% at the end of Q3 2020, having further decreased from 2.6% in Q2 2020. In view of no new delivery, warehouses scheduled for delivery in Q4 2020 are already partially or fully pre-leased.

Major warehousing and logistics properties scheduled for completion in the Greater Kyiv area in Q4 2020 – 2021

|

Property |

Location |

Area*, sq. m |

Owner / Developer |

|

Office and logistics complex ‘Makarivskyi’ (phases 1-4) |

M-06, E40 |

61,992 |

ADG |

|

Amtel Logistics Complex (phase 2) |

Kyin Ring Road |

53,000 |

Amtel Properties |

|

FM Logistic (phase 4) |

Brovary-Boryspil RR |

17,000 |

FM Logistic |

|

Warehouse |

M-06, E40 |

9,500 |

Local developer |

* Including ancillary office and mezzanine space.

Source: Cushman & Wakefield

Rents

After continuous rental growth in 2017-2019, in Q1-Q3 2020 base monthly rents for quality warehousing space were generally stable in the US dollar equivalent, being in the range of USD 4.0-5.8 per sq. m for prime warehousing space in H1 with some decrease in Q3 2020 due to currency depreciation, and at around USD 3.0-3.5 per sq. m for the highest quality B class properties. In a number of properties with UAH denominated leases base rents decreased in the US dollar equivalent due to the hryvnya depreciation by over 19% since the year start.

Prime logistic rent and market vacancy

Source: Cushman & Wakefield

“It is obvious today that the warehousing and logistics property market is one of the most promising not only in Ukraine but also in the world. The premises for this conclusion were formed even earlier, despite the gradual demographic changes and the evolution of approaches to trading, but the consequences of the COVID-19 pandemic accelerated this process in light of quarantine measures in many countries and the growing importance of e-commerce and delivery speed, said Marta Kostiuk, Head of Research and Development Consultancy at Cushman & Wakefield. - Despite the economic downturn and the current crisis, the demand for professional warehousing property is high, and its growth in the Kyiv region is limited by the record low vacancy in the sector. Despite the obvious prospects, we also observe a high interest in the warehousing and logistics property market in Ukraine from developers, investors, and financial institutions. The main cities on the market players’ radar are now not only the Kyiv region but also Lviv and other cities with a population of over one million, in particular, Kharkiv."