- Rental growth is accelerating across Europe with further yield compression.

- Annualised European logistics rents grew to its highest rate in over a decade.

- However, retail yields set to move out in over 40% of markets with nil or negative rental growth in 2019.

Europe’s commercial real estate markets maintained their positive trend across most markets and property types during the fourth quarter of 2018, according to Cushman & Wakefield’s latest DNA of Real Estate report.

Nigel Almond, Head of Data Analytics at Cushman & Wakefield, commented: “The office and logistics sectors were the main engines of growth during the fourth quarter – as they were across 2018 as a whole. At the European level, office rental growth accelerated by an annualised 2.6%; its strongest annual rate in over five years. Rental growth in the logistics sector also experienced its strongest annual rate of growth in over a decade, by 2.3%.

“Meanwhile, the retail sector across Europe was more subdued, with rents falling 0.1% over the quarter. Nonetheless, it was an improvement on the 0.4% fall in Q3 and was just about enough to push annual rental growth into positive territory over 2018.”

Yields also continued to compress across Europe, with the strongest movement remaining in logistics; down 20bps in Q4, driven by the strong investor demand and rental growth. Office yields compressed a further 6bps, with retail down just 2bps.

Budapest was the only market of the 46 cities tracked by Cushman & Wakefield to experience both positive rental growth and yield compression across all property types in Q4, supported by strong economic fundamentals and occupational and investor demand. High Street retail rents rose 7.1% in Q4, which was driven by strong real earnings growth, consumption and the increasing popularity of high street retail fuelled by tourism. Logistics rent grew for the seventh consecutive quarter (+2.4%) reflecting rising construction costs and low availability of warehouse space.

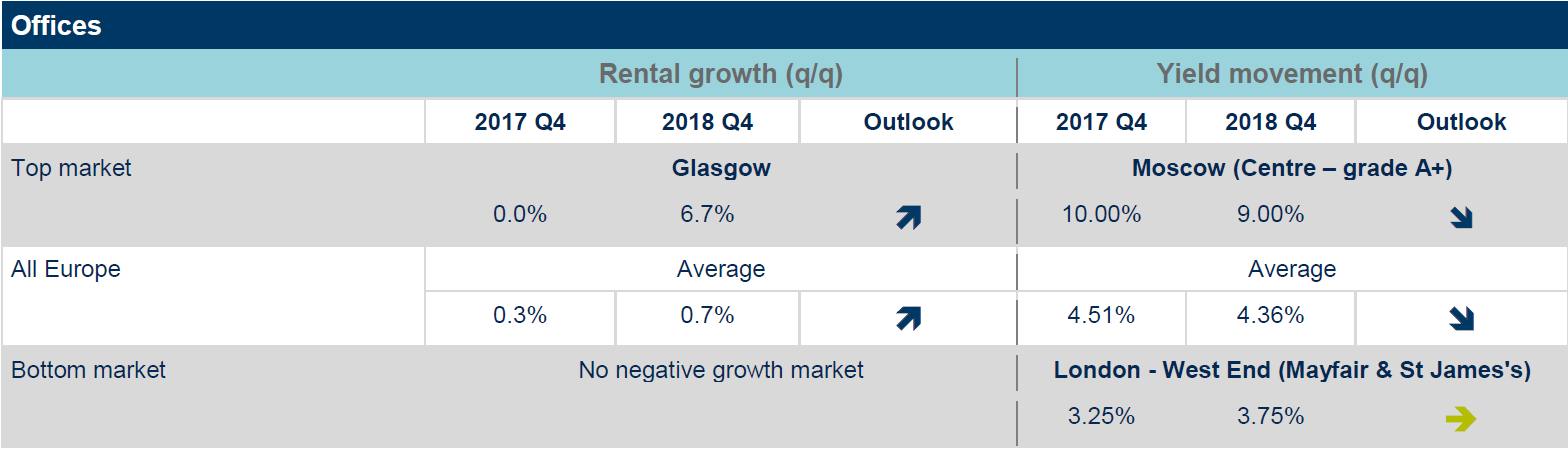

Offices

European office rents continued to grow in Q4 2018 by 0.7% (+2.6% y-o-y). No rental decrease was recorded in any of the markets tracked. Furthermore, 15 out of the 47 monitored markets had some level of rental growth in Q4, led by Glasgow (+6.7%), Barcelona (+3.9%) and Brussels (+3.3%). Rental growth in the office sector has been the most consistent throughout 2018 with over 0.5% quarterly growth in all four quarters.

The highest annual growth was recorded in Barcelona (+15.2%) due to shortage of high quality office supply, followed shortly by Berlin (+13.8%) where the economy was robust, and demand was strong with low supply. Elsewhere, strong leasing activity coupled with falling vacancy rates for quality new space caused prime rents in five UK regional offices to increase in 2018. In Italy, a record level of office take-up drove rents up 7.4% in Milan and by 5% in Rome during the past 12 months.

The overall European office yield was 6bps lower in Q4 to 4.36%. Germany (-26bps), Benelux (-22bps) and CEE (-36bps) all recorded substantial compression in the past 12 months. Yields appear to have reached their floor in France, while semi-core and Nordic markets have seen more limited compression over the quarter and the year. The UK office yield rose over the quarter and the year primarily as London West End prime yield moved out 25bps to 3.75% in Q4.

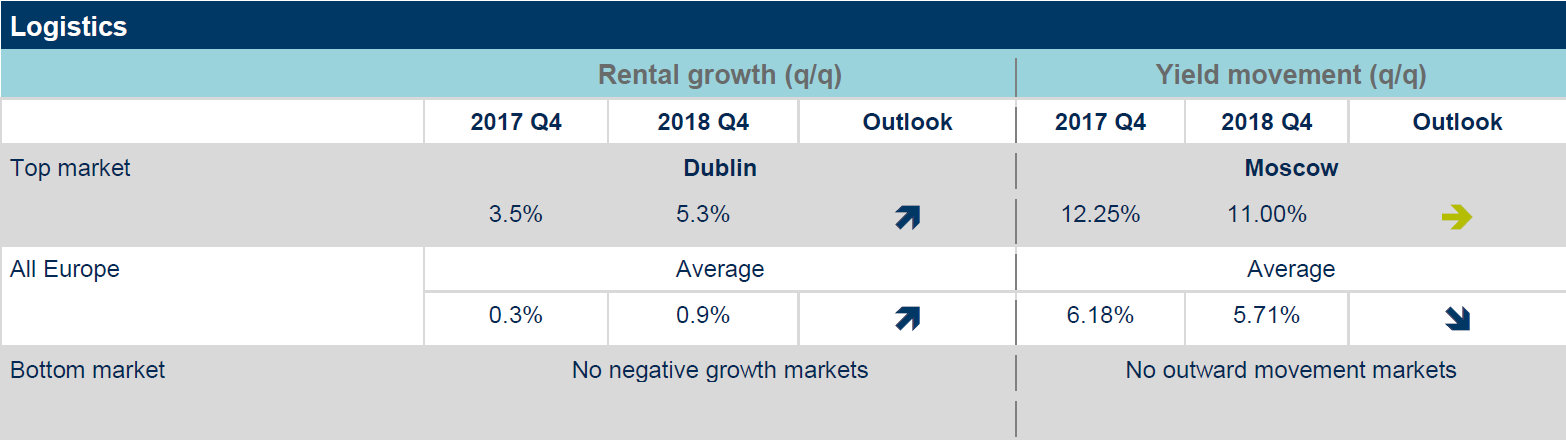

Logistics

Logistics rents across Europe continued their upwards trend rising 0.9% over Q4 2018 and up a stronger 2.3% over the year. Close to half of the 46 markets tracked registered growth over the course of the year, although growth was recorded in fewer markets in Q4; primarily Dublin (+5.3%), London (+3.3%), Moscow (+2.9%) and Budapest (2.4%).

Meanwhile logistics yields fell in more than half of the tracked markets. Overall European logistics yield was down by 20bps to 5.71%, which is the biggest movement in over three years. At the country level the biggest quarterly movement in yields was seen in German (-38bps), Belgian (-25bps), Italian (-25bps), and Dutch (-23bps) markets. Strong demand, relatively limited supply and expected rental growth continues to propel logistics yields lower in many markets.

Almond added: “The solid rental growth and yield compression recorded in the logistics sector during Q4 is a continuation of the fine performance of this sector over the past 12 months. Logistics property, in general, is under-supplied in many markets and this applies to both leasing and capital markets. We can expect further rental growth in 2019, but we anticipate yield compression to be slower.”

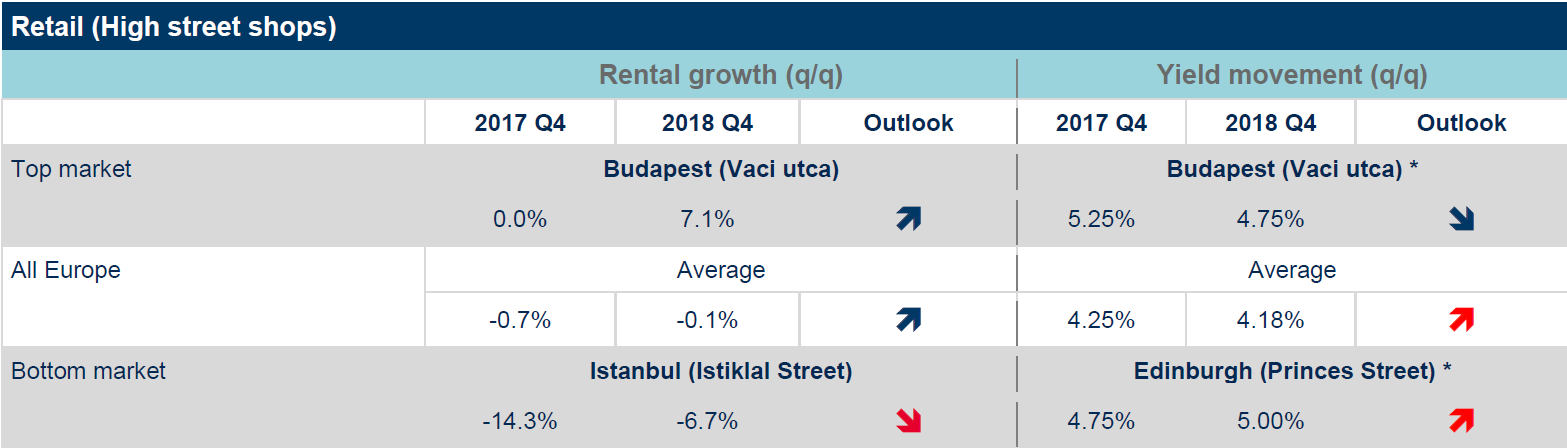

High Street Retail

European high street retail rental growth remains subdued, falling 0.1% over the quarter, but largely stable over the year. Rents were stable in over 80% of markets tracked in Q4, with growth limited to a handful of markets in CEE (Budapest +7.1% and Sofia +4.0%), semi-core (Rome +4.3% and Barcelona +1.8%) and in the UK (Leeds 2.0% and Manchester 1.8%). With rents flat in more than half the markets over the year, and growing concerns over online shopping, rents are likely to remain subdued in the near term with rents predicted to be flat or negative in over 60% of all markets in 2019.

These concerns are impacting investor sentiment with high street yields again the weakest of all use types, edging in just 2bps in Q4. CEE markets of Budapest and Sofia, which benefitted positive rental growth over the quarter, saw yields edge in 25bps. Notable movement was also evident in Warsaw (-25bps) and Amsterdam (-15bps). Yields have already moved out in nearly a quarter of the markets monitored this year, including Edinburgh, Glasgow and Oslo (+25bps) and Brussels (+10bps) this quarter.

Almond said: “Given many yields are at 10-year lows and the strong likelihood of negative or minimal growth, we foresee yields moving out in up to 40% of all monitored markets.”