I. FOREWORD

Transactions have ranged in structure and style across a series of sectors from distressed banking asset sales to growth-oriented strategic purchases in energy and TMT.

The government of President Petro Poroshenko has pushed an ambitious reform agenda, designed to overhaul the investment climate and attract more foreign and domestic capital. Anti-corruption moves, reform of the tax code, and radical energy sector changes have all figured prominently and have alerted foreign acquirers to the untapped potential of one of Europes largest countries.

The implementation on 1 January 2016 of the EU Association Agreement adds further ballast to the pro-reform, pro-business agenda. This should pivot the economy more firmly westwards - a welcome diversification that can only strengthen an economy that has suffered in recent years from its historical connection with Russia. Meanwhile, the International Monetary Funds (IMF) financial support has extended a lifeline to the government.

However, some sizeable challenges still need to be met. Economic growth is still fragile, and Ukraine has hard work ahead of it in meeting the terms of the IMF support programme. The situation in the Donbas region is a concern and the reform initiatives remain a work in progress. And yet, a look at some recent activity suggests investors are conident that the right steps are being taken and that some solid business opportunities are emerging.

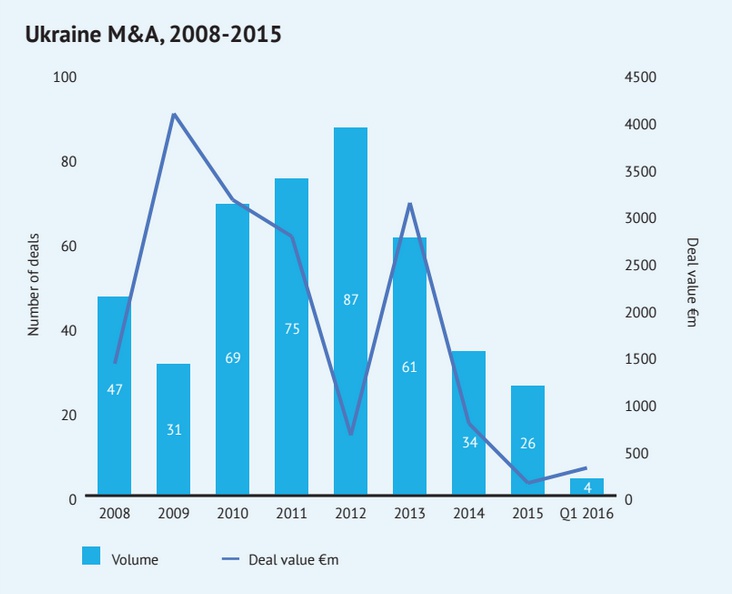

Dealmaking opportunities in 2016 appear robust. Although deal volume dropped by 24% in 2015 to 26, with disclosed value down from €768m in 2014, the expectation is that 2016 will show a marked improvement. Last year, there were standout deals in both traditional sectors such as the sale of a large stake in Kub-Gas for €20m by Canadas Serinus Energy and within the new economy arena including US developer Snapchat buying Odessa-based start-up, Looksery, in a deal that showcased a formidable nascent tech sector talent pool.

Consolidation of banks has bolstered balance sheets and made for some appealing buying opportunities in the inancial services sector (which last year accounted for more than one-third of overall M&A activity). Private equity buyouts remained slow in 2015 with just two deals, but sectors such as pharmaceuticals, medical and biotech (PMB) are proving attractive to PE funds, whether domestic or foreign. The expectation is that PE investors with healthy risk appetites will be in the vanguard of dealmaking in Ukraine this year.

Ukraines business community continues to send out the message that the country is open for business, and that good deals can be snapped up by the eagle-eyed and nimble-footed.

II. M&A OVERVIEW IN UKRAINE

In challenging geopolitical circumstances, 2015 nonetheless demonstrated the resilience of Ukraines dealmaking. There was sufficient activity to allow for cautious optimism that the market has seen the bottom of the valuation curve and that 2016 should see an upward turn with more willing buyers and sellers coming to the fore.

The figures show that M&A in 2015 was quieter than in previous years. However, political unrest notwithstanding, the prospects for a rebounding economy and dealmaking opportunities in 2016 look decent. This dynamic is similar to the slump in M&A after the 2008-2009 financial crisis, which was followed by a spike in dealmaking in 2010.

THE ECONOMIC BACKDROP

Deal volume in 2015 decreased by 24% to 26 and disclosed values reached €134m ($150m), compared to €768m ($831m) in 2014. These igures tallied with the countrys economic downturn, which was in turn affected by the challenging political context caused by the Russian military engagement in the east of the country. Indeed, Ukraines economy is estimated to have contracted by 12% in 2015, according to a World Bank report issued in early January.

However, in more optimistic news, a turnaround is expected in 2016. The aforementioned World Bank report states that the economy is on course for a modest rebound with growth of 1% in 2016 and 2% in 2017 and 2018. This would be supported by an easing of the armed conflict in the east and continued progress on its IMF-backed reform programme, the World Bank forecasts.

In addition, Ukraines inflation should ease to 12% at the end of 2016, from an estimated average of 45.8% in 2015, the IMF predicts. The Ukrainian authorities endeavour to implement an IMF-backed stabilisation program, and fiscal consolidation is ahead of targets noted in the four-year IMF programme agreed in March 2015, which included a payment of $5bn in 2015.

However protracted the political situation, efforts have been made to stabilise the economy with the support of the IMF and private creditors and the extension of bond maturities to 20192027. Ukraine reached agreement on an $18bn private debt restructuring deal in September 2015 that includes a 20% write-down for creditors, though a debt dispute with Russia continues after the government announced a moratorium on $3bn in bond repayments due to Russia in December 2015.

HOPE FOR 2016

Overall, these efforts provide a supportive climate for M&A activity in 2016 and beyond. Subject to the continuing stabilisation at the macro level, experts expect more investment in the Ukraine this year.

One key development, which came into effect on 1 January, is the long-anticipated Deep and Comprehensive Free Trade Areas (DCFTA) with the European Union (EU). The DCFTA - an advanced form of association agreement - will offer Ukraine a framework for modernising its trade relations and for economic development by opening markets through the progressive removal of customs tariffs and quotas, and by an extensive harmonisation of laws that will bring Ukraine up to European standards.

This is one of the factors that will underscore more positive sentiment in 2016, as the EU remains Ukraines largest trading partner, accounting for more than one-third of its trade. This agreement will shift Ukraines export markets west. Since the EU is the main source of FDI into Ukraine, the DCFTA provides an opportunity to make the country more competitive.

The green shoots of Ukraines recovery can be traced back to September 2015, says Anna Babych, a partner at Aequo, who points out the irm has seen a sharp rise in the number of requests for proposal for M&A in recent months, from foreign law firms and from local players. Broadly, there are two types of M&A deals in Ukraine - foreign-to-foreign transactions, which are larger in size, and the purely mid-size local deals. The latter tend to be mid-sized deals of the $20m-30m magnitude.

"Foreign-to-foreign deals are more frequent now," says Babych. Although the M&A activity has been undermined by the economic downturn, there is a strong impression that Ukraine has passed the bottom of the cycle."

III. SECTOR WATCH

Although M&A activity was muted in the country in 2015, some sectors were more resilient than others. In particular, financial services and energy, mining and utilities were robust, particularly in value terms. Here, we drill down into four key industries as well as examining the outlook for the private equity (PE) sector.

FINANCIAL SERVICES

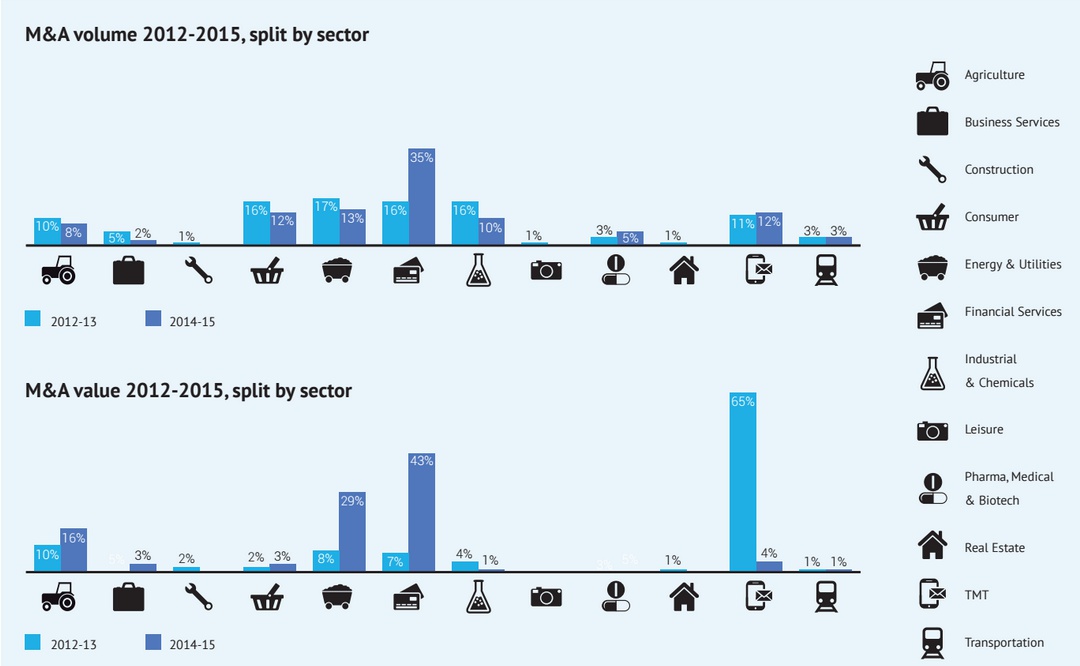

In sectoral terms, inancial services has come to make up a higher proportion of M&A deals than has historically been the case in Ukraine. Financial sector deals in 2014-2015 made up 35% of total M&A volume, compared to 16% in 2012-2013, and jumped to 43% of total M&A value compared to 7% in 2012-2013.

There have been a number of acquisitions of distressed banks. In an EBRD-sponsored project, Aequo advised the Deposit Guarantee Fund and the National Bank of Ukraine (NBU) in preparing legislation on how to deal with insolvent banks and sell them on to new investors. This is one indication that foreign buyers believe that Ukraines banking sector has progressed beyond bankruptcy risk, with non-performing loan losses largely accounted for and balance sheets steadily cleaned up. That provides a much clearer perspective for prospective acquirers about the health of Ukrainian banks.

The summer months of 2015 were particularly busy for the financial services sector. In August, UAE-based Primestar Energy acquired 100% of UkrGazPromBank, declared insolvent in April 2015.

Earlier in mid-July, Agro Holdings, owned by the US-based PE firm NCH Capital, acquired a 100% stake in Astra Bank, a lender that had been announced insolvent in March 2015. As a result of the investment, Astra Bank received the cash injections it needed to restore its capital adequacy and liquidity levels.

The transaction was the irst ever purchase of an insolvent Ukrainian bank from the Deposit Guarantee Fund (DGF), and was advised by Aequo on the buyer side.

The banking system is going through transformations led by the National Bank of Ukraine. We have cleaned up the banking sector from the old legacy and thus made it healthier. Dozens of banks have passed through the capitalisation phase and banks that didnt manage to duly capitalise have been removed from the market. The NBU tightened the control over transactions with parties related to banks and made the banking sector more transparent by enforcing disclosure of the banks ultimate beneficiaries. We have considerably enhanced the legislative basis for liability of the banks managers and owners for failing to provide support to their banks. The NBU is pushing for banking sector consolidation and expects up to 20 banks to participate in mergers in 2016."

Vladyslav Rashkovan, Deputy Governor of National Bank of Ukraine

Shortly after, the DGF announced the acquisition RWS, a bank established from the insolvent Omega Bank, by the Ukrainian Business Group, also advised by Aequo in the transaction.

Aequo was later noted in the Financial Times Innovative Lawyers 2015 report for these transactions, as well as assisting the EBRD on the launch and implementation of state insurance of household deposits and bank reforms, which ranked among the most innovative deals in finance in Europe, and "helped stabilise the Ukrainian financial market following the outbreak of the conflict in 2014."

More recently, in January 2016, UniCredit Group agreed to transfer its stake in Ukrsotsbank to ABH Holding, owned by Russias Alfa Group. The Ukrsotsbank-Alfa merger creates the countrys fourth biggest credit corporation. In exchange, UniCredit will receive a 9.9% share in ABH

Holding. This leaves Alfa Group in charge of two of Ukraines top banks by assets, Ukrsotsbank and Alfa Bank.

More such deals may be in store, says Lysenko. "In terms of numbers there will be more inancial services deals, some of them being of a type that was seen in 2015, as with the sale of two distressed banks by the Deposit Guarantee Fund," he says. "The two deals were on behalf of buyers who were looking for a bank to turnaround. Those were successful and there could be more to follow, although that is dependent on appetite from investors already familiar with the Ukrainian market."

The UniCredit deal was effectively a share swap arrangement, whereby the local subsidiary of UniCredit was contributed in kind, a nonmonetary mechanism that might figure more often in future deals. "UniCredit receives a

consideration for its Ukrainian subsidiary at the level of the Alfa regional business, and this is a trend we could see in larger deals," says Lysenko. "The buyer was prepared to offer consideration in stock rather than paying full price in cash."

Domestic consolidation in the financial services sector continues to strengthen banks and insurers. For example, the European Bank for Reconstruction and Development (EBRD) increased its stake in UkrSibbank through underwriting a €120m ($130m) capital increase, announced in mid-October 2015. The shares are distributed between the banks current shareholders: BNP Paribas and EBRD, overall the biggest foreign investor in the Ukrainian economy.

ENERGY, MINING AND UTILITIES

For a richly resource-endowed country, energy will always igure prominently in M&A activity in Ukraine. It made up 29% of all M&A in 201415 by value and 13% by volume. And there is still potential for growth moving into 2016 and beyond. The natural gas market is opening up, new infrastructure is being created and state-owned Naftogaz is actively trading and buying imported gas from the EU in competition with Ukraines traditional supplier, Russia.

Last years third-largest announced deal with disclosed deal value was the sale of 70% stake in Kub-Gas for €20m ($21.7m) by exploration and production (E&P) company Canadian Serinus Energy. The latter said in December 2015 that it had reached an agreement to sell its 70% stake, with Texas-based Cub Energy, the owner of a 30% stake in Kub-Gas, exercising its right of first refusal to buy the remaining 70% stake in the Ukrainian company. The sale was triggered by the death of one of Kub-Gass major shareholders.

Low valuations of local energy and resource companies - driven by record-low oil prices -create a compelling incentive for buyers to pick up assets at rock bottom prices. "Discussions are underway precisely because of the low valuations," says Lysenko. "But with the oil and gas price trend unpredictable and limited inancing opportunities for buyers, I expect most will likely be forced deals."

There have been some dramatic changes in the regulatory environment in oil and gas and the electricity market, which will add heft to the energy market reshaping. In late December, changes have been made to the tax code, which included more than halving the natural gas production tax for private exploration and production companies in 2016. The law envisages tax rates for private gas producers will decrease to 29% from 55%, and to 14% from 28% (for gas mined from wells deeper than 5,000m). The tax base would also change, switching from a marginal price set at $225/trillion cubic metres to the average import price of gas (expected to be about $210/tcm) in Q1 2016. A new tax regime for gas E&P irms would be implemented from January 2018, and would see the production tax rate reduced to 20% (and 10% for deep wells), while an additional 15% surcharge to the proit tax will be imposed on the difference between a companys revenue from natural gas sales and capital expenditure into E&P.

"The reduction in royalties is a good sign because investors will now be looking at potentially renewing investment projects that were previously suspended" says Lysenko.

In the electricity market, new tariffs have been set for both industrial and individual consumers with substantial increases that could make utility companies more appealing as potential acquisition targets. Earlier, the price for consumers was 0.37 Ukrainian hryvnia (UAH) per kWh. From September 2015, it was hiked to 0.456 UAH per kWh.

Ukraines new gas market law came into force in October 2015, harmonising national legislation with the EU establishing common rules for the domestic market and for access to gas transmission networks. That will also underpin conidence in dealmaking prospects in what is becoming a much more competitive market, where consumers are able to choose suppliers. "In all likelihood," says Lysenko, "most M&A activity in energy will still come from those investors already present in Ukraines market.

In the past, privatisation deals have igured in the energy sector, and that will likely prove the case in future. In 2014, two electricity distributors, PAT Vinnytsyaoblenergo and PAT Zakarpattyaoblenergo saw 25% stakes sold respectively. This trend is to continue with the sale of energy generator Centrenergo in Q2-3 2016, and the expected sale of stakes in several distributors. Centrenergo is Ukraines second-largest thermal generator by capacity and operates three power plants in the industrialized Kyiv, Kharkiv and Donetsk regions. Three companies with US capital are said to be among potential bidders for the utility, while other foreign interest is reported to have come from Gaz de France.

The government has said it will make it a priority to sell minority and majority stakes in electricity distribution companies. "The next phase of reform will see the breaking up of regional energy monopolies, and a restructuring of the distribution companies," says Lysenko. "These networks require investment but have the potential to attract investors, subject to the ratification of energy market reforms."

TELECOMMUNICATIONS, MEDIA AND TECHNOLOGY (TMT)

TMT is the third most active M&A segment in Ukraine, appealing strongly to both private equity and strategic investors. Last years standout deal saw US developer Snapchat buy the Odessa-based start-up Looksery, which develops mobile apps using facial recognition technology, for €132m ($150m).

The company is registered in the US so technically it was not an inbound deal but was developed in the Odessa office and showcased Ukraine-based programming talent - something that has piqued global interest in the last couple of years. An earlier deal involving another Ukrainian facial recognition technology firm Viewdle, resulted in the company being acquired in 2012 by Google-owned Motorola Mobility for an estimated €42m ($45m).

Telecoms deals have also featured prominently. In June 2015, Turkeys mobile operator Turkcell agreed to buy 44.96% of shares of Ukraines SCM Group in the Eurasia Telecommunications Holding BV (Netherlands), which owns 100% of the Ukrainian mobile network operator lifecell (formerly life:) for $100m. Turkcell was also said to have started negotiations last year for the purchase of Ukrtelecoms 3G-division TriMob. Russian mobile operator MTS is also looking at acquiring TriMob and is reported to have made a bid in early 2016 estimated at €114m ($123m), having last year sold a part of its ixed-line business to Ukrainian conglomerate System Capital Management. Advisers expect at least one large deal to develop soon in the telecom sector. "There might be more to come, but much will depend on valuations. Overall, the situation is favourable for investors as telecom operators are increasing capacity in 3G networks and are expanding regionally," says Lysenko.

Foundation, acquired Danish IT and software services provider Ciklum from Horizon Capital and Majgaard Holdings for an undisclosed sum. The company was founded in 2002 by Danish citizen Torben Majgaard in Kyiv. The investment by URF will fund Ciklums focus on growth in the UK and US markets and signals positive momentum for the already competitive Ukrainian technology segment and the countrys software and programming talent. Babych, who advised on the acquisition, describes it as a benchmark deal for the country, adding that there are other good outsourcing companies that may attract investors. "This transaction is the first of its kind in the Ukrainian IT sector and the first official big deal by a PE fund involving Ukraine after the events of 2014. It can play an important role in attracting other private investors, especially from Europe and North America, to the emerging IT services market in Ukraine," says Babych.

One of the largest TMT deals in 2015 was a private equity deal. In a deal sealed at the end of the year, the Ukrainian Redevelopment Fund (URF), associated with the George Soros Foundation, acquired Danish IT and software services provider Ciklum from Horizon Capital and Majgaard Holdings for an undisclosed sum. The company was founded in 2002 by Danish citizen Torben Majgaard in Kyiv. The investment by URF will fund Ciklums focus on growth in the UK and US markets and signals positive momentum for the already competitive Ukrainian technology segment and the countrys software and programming talent. Babych, who advised on the acquisition, describes it as a benchmark deal for the country, adding that there are other good outsourcing companies that may attract investors. "This transaction is the first of its kind in the Ukrainian IT sector and the first official big deal by a PE fund involving Ukraine after the events of 2014. It can play an important role in attracting other private investors, especially from Europe and North America, to the emerging IT services market in Ukraine," says Babych.

AGRICULTURE

The farming sector has long been Ukraines bread and butter industry, with a steady stream of transactions in this sector, but many deals are not captured as values often remain undisclosed. One of the bigger deals was US-based agribusiness Cargills €146m ($200m) investment in a 5% stake in the countrys leading agriculture group Ukrland in 2014, which preceded four deals in 2015, two of which were inbound from Austria and Germany. Cargill has been active in Ukraine for over 20 years, operating two big sunflower oil plants and several silos.

The agricultural sector was one of the top sources for Ukraines export revenue in 2015. The sectors prospects have been dimmed in light of Russian recession, which has crimped demand for Ukrainian produce. "Much will depend on the EU DCFTA" says Babych. "That will test to what extent Ukrainian agriculture exports can benefit from the agreement, and whether those food producers that have historically traded with Russia can adapt."

Despite the inclement economic conditions, last year saw several key agribusiness deals. For example, in March, US-based OSI Group sold two affiliates, Agrobeef and Agrosolutions, to an undisclosed German bidder.

iV. FOCUS: PRIVATE EOUITY IN THE SPOTLIGHT

Much like its corporate counter-part, the PE sector has slowed somewhat in the last two years. In 2013, there were eight PE deals, which slowed in 2014 to one exit and one buyout and bumped back up to two buyouts and one exit in 2015.

However, certain sectors such as TMT are proving a magnet for PE investors and give reason for cautious optimism about prospects for deals involving private equity investors in 2016. In July 2015, the Emerging Europe Growth Fund II, the Ukraine-based private equity fund of Horizon Capital, acquired an undisclosed stake in Rozetka.ua, the Ukraine-based e-commerce company, for an undisclosed consideration.

Ukraines e-commerce recorded growth rates of more than 30% in the last ive years, in US dollars, and still retains signiicant upside potential as both internet penetration and online shoppings share of total retail remain substantially lower than regional peer levels. Indeed, online penetration currently sits at 43%, below neighbouring countries such as Poland, Belarus and Moldova. Lenna Koszarny, CEO of Horizon Capital, said at the time of the deal that Ukraine offered a true ground-loor opportunity for investors in Ukraines rapidly-growing knowledge economy.

The Ciklum deal (see TMT section, page 11) was another sizeable PE-related deal that broke the mould. One big advantage of PE investors, says Babych, is that their greater risk appetite encourages strategic investors to take more risks. PE funds have picked up a number of distressed assets, including insolvent banks.

Pharma and medical businesses also yield interesting targets for PE firms. For example, a Russian buyout firm focused on the region and, with previous investments in Ukraines healthcare sector, is nearing completion of a deal to buy Kyiv-based medical clinic group Medisvit for an estimated €5m. "We have seen deals at low valuations, and there might be more to come in the pharmaceuticals sector as the market consolidates," says Lysenko.

Overall, Lysenko expects more PE activity in 2016, in the mid-cap range. "We are not expecting any large deals to happen in this environment. The level of funding which may be committed at this time for Ukrainian projects will be limited, even if the targets look attractive."

V. THE OUTLOOK FOR 2016 AND BEYOND

From distressed asset sales to government privatisations, the next year should throw up some interesting opportunities for buyers with an interest in Ukraine. Below are five points that could drive deals in to the country.

1. PRIVATISATIONS: State sell-off plans have been underway for some time, with the government seeking to privatise half of all state-owned businesses, including the most strategic ones. The government is targeting as much as $2bn in privatisation revenues in 2016, having in past years postponed a series of such sales.

This list of state-owned enterprises is topped by the likes of fertiliser company Odessa Port Plant (Odeskyi Pryportovyi Zavod - OPZ), energy company Centrenergo and agricultural machinen leaser Ukragroleasing. Privatisation reforms received parliamentary approval in early 2016. "Reform of SOEs is one of the key issues facing Ukraine. There are more than 3,000 SOEs in Ukraine and only half of them are working - the rest are either insolvent or dormant. Out of these 1,500, most should be privatised to improve their efficiency, leaving just 200-300 SOEs in state hands" comments Babych.

However, there are only between 30 to 50 SOEs that are of major interest to foreign investor - like OPZ. OPZs sale was set for Q2 2016, the auction having been put back from November as Ukraines privatisation authority, State Property Fund (SPF), pushed for new legislation to make the assets more attractive. That was shelved in late 2015 as MPs failed to agree to modify certain procedures.

Officially, SPF is planning to put up for sale stakes in 88 state enterprises in 2016, 34 controlling stakes, including over 99% shares in chemicals plants OPZ and Sumy-Khimprom, 78.3% of Centrenergo and 50%-70% stakes in four power distribution companies, and 99%+ stakes in four heat and power plants. The list also comprises 25%-50% stakes in 31 companies, including 25% in five power distribution and generation companies.

Whether these will transpire according to plan is a moot point. "This year looks like a transition year" says Lysenko. "One potential way forward would be to jumpstart the long-delayed privatisation process. Recently enacted changes to the privatisation procedures will ensure that the valuations that the government is expecting can be obtained."

Those procedures should not give inappropriate advantage to local interest groups with a history of investing in state assets, and who know how to get their foot in the door by buying very small stakes in state companies.

Investors are waiting for the privatisation of large Ukrainian companies, and the government understands the significance of private investors for Ukraines prosperity. There is a strong will to ensure professional and transparent large-scale privatisation, from announcement to auction. This is a win-win situation. Anti-corruption efforts and the adoption of a law on privatisation by the Ukrainian Parliament will unlock the privatisation of state assets."

Igor Bilous, Head of the State Property Fund of Ukraine

2. UNLOCKING BUSINESS: More needs to be done to open up the countrys undoubted commercial potential. Certain aspects of starting a business are easier than in other European and Central Asian countries, but in the Doing Business Index the Ukraine is still ranked lower than many other European countries at 83.

Judicial reform with constitutional changes has been initiated over the past year, in a broader strategy of strengthening of legal institutions and yielding a positive impact for those seeking to do business in the Ukraine. Changes to the judicial process seek to make it more independent while putting a check on corruption.

3. TAX REFORM: A revised tax code was endorsed in late 2015 and that now forms the basis of the 2016 state budget. More far-reaching amendments to the tax code expected to be approved in 1H 2016 would overhaul the current, highly complex tax system that comprises 97 different national rates and puts a greater burden on SMEs compared to large business. A proposed simpliied system would need to set lower rates for income tax, corporate tax, social security contributions and potentially VAT, in an effort to improve collection rates. Any reductions in the tax burden would be funded within the state budget to keep Ukraine beneath the 3.7% deficit ceiling set out in the IMFs four-year support programme.

Tax reform is critical for foreign investors, says Babych: "Without clarity on how much tax they will be liable for, this will remain a hidden risk for investors until the reforms are implemented."

4. COUNTERING CORRUPTION: A series of anti-corruption laws have been introduced since 2014, establishing a set of institutions to fight graft. Judicial processes are being improved to allow for more transparency and better public oversight of corruption cases. Prosecutors are encouraged to be more active in rooting out anti-corruption activities. New agencies such as the National Anti-Corruption Bureau and the National Agency for Prevention of Corruption have been set up, with representatives from all branches of government. However, a comprehensive set of constitutional amendments to be supplemented by draft laws on judicial reform is awaiting approval in the parliament. These would bring in changes in the selection, promotion and prerogatives of judges, and strengthen the independence of the judiciary.

"Transparency and constructive communication with business and fostering competition are the main priorities of the Antimonopoly Committee of Ukraine. Ongoing reform of the competition legislation, including the increase of financial thresholds requirements for merger control, transparent guidelines for fines calculation, publication of the regulators decisions and other recent steps taken by the Antimonopoly Committee of Ukraine are primarily focused on advocating competition and improving the investment climate in Ukraine."

Yuriy Terentyev, Chairman of Antimonopoly Committee of Ukraine

5. MINORITY AID AND MERGER CLEARANCE: Other improvements have seen greater protection for minority shareholders introduced. Aequo is advising the Ministry of Economic Development and Trade on drafting legislation on limited liability companies, updating an existing law that dates back to 1991. "On top, elements such as merger clearance issues have been addressed by the early 2016 EU-backed legislative updates, as historically we have had low thresholds. Adoption of the respective law is a long-awaited event in Ukrainian competition circles being a part of the systemic reform of Ukrainian competition legislation," says Babych.

VI. CONCLUSION: OPEN FOR BUSINESS

With just €134m ($150m) in disclosed deals last year, Ukraines M&A market has the benefit of knowing that the only way is up. Few will look back fondly on a tough economic year for Ukraine in 2015. It was a year in which regional political events largely overtook the positive sentiment evident two years previously after the Euromaidan protests heralded a transformation of the country. However, there is much to underpin the conidence among advisers and dealmakers that 2016 will bring better news, with more deal activity in the pipeline and the prospect of reform embedding itself. That can only point towards a far more attractive investment climate for nationals and foreigners alike.

Although M&A volumes fell by 24% in 2015, this was largely for the same reasons that dealmaking fell back in the aftermath of the late 2000s financial crisis, which was also followed by a spike in activity. Financial services, accounting for 43% of deal values over the past two years, reveal an opportunity for those willing to establish a foothold. Local banks, after sector consolidation and recapitalisation efforts, are gradually starting to lend again which strengthens the overall business climate in the country.

The biggest structural challenges to deal activity - the sense that well-positioned local investor groups have enjoyed in-built advantages; the prevalence of opaque tax regimes; an uncorporatised state-owned enterprise sector; and fluctuating commodity prices thwarting visibility on valuations - are being addressed. Once privatisation procedures are inalised, a raft of corporatised state-owned enterprises (SOE) will eventually be presented to investors, some of them concentrated in value-added sectors such as petrochemicals, technology and transport, that have solid future growth potential. Now that the most optimistic scenario is being implemented, as the Ukrainian parliament has given the necessary support to the privatisation changes in Q1 2016, the process could get underway as early as late 2016.

Some private equity investors have acquired a taste for Ukrainian risk recently, and will likely re-establish themselves as more active buyers in coming years.

At the political level, there is cautious optimism that the situation in Donbas will stabilise, and that a resolution of the military conflict is in reach. And Ukrainians are quick to point out that Donbas only accounts for about 5% of the countrys total territory; the country is still very much open for business. Moreover, the DCFTA with the EU that came into effect in January will help rebalance Ukraines economy away from its large, recession-bound neighbour. Improved access to the EU market will give a substantial boost to European-Ukrainian deals, and the IMFs financial support - tied to much-needed fiscal and anti-corruption reforms - will help keep the countrys inances on a stable footing.

If the outlook for 2016 is still subject to caveats and caution - some of that linked to conditions in the global economy that are beyond Kyivs immediate control - there is a palpable feeling among Ukraines dealmakers that better things are in store in 2016. For those prepared to stay the course, do the due diligence, engage with Ukrainian partners and establish irm roots, the going is likely to get a lot better in 2017. And those who have the benefit of first-mover advantage are likely to be best placed to accrue the results once Ukraine succeeds in pivoting towards Europe, and entering the continents business mainstream.

Source: AEQUO, Mergermarket

Denis Lysenko / Managing Partner, M&A / Antitrust & Competition, Tax

Anna Babych / Partner, M&A, Corporate / Capital Markets