Key Trends in Kyiv Warehouse Real Estate

- A record gross take-up of 217,000 sq m was recorded (+30% y/y), driven by the activity of major retailers and 3PL operators.

- 216,000 sq m of new warehouse space was commissioned, fully restoring total supply to the pre-war level of 1.57 million sq m.

- The vacancy rate declined to 3.5% (-0.3 pp since the beginning of the year), reflecting the active absorption of pent-up demand.

- The prime rental rate remained stable at $5.3/sq m/month (excluding VAT and OPEX), in line with pre-war levels.

- The total volume of new supply projected for 2026 is estimated at around 90,000 sq m.

Demand for Kyiv Warehouse Real Estate

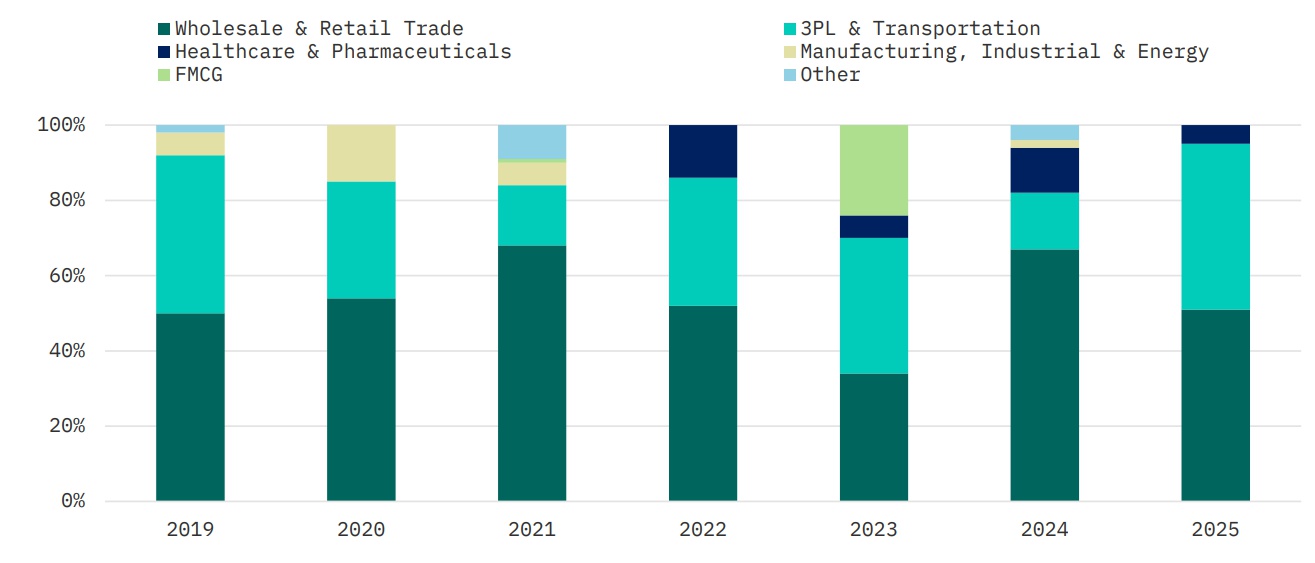

By-Industry Leasing Activity, 2025

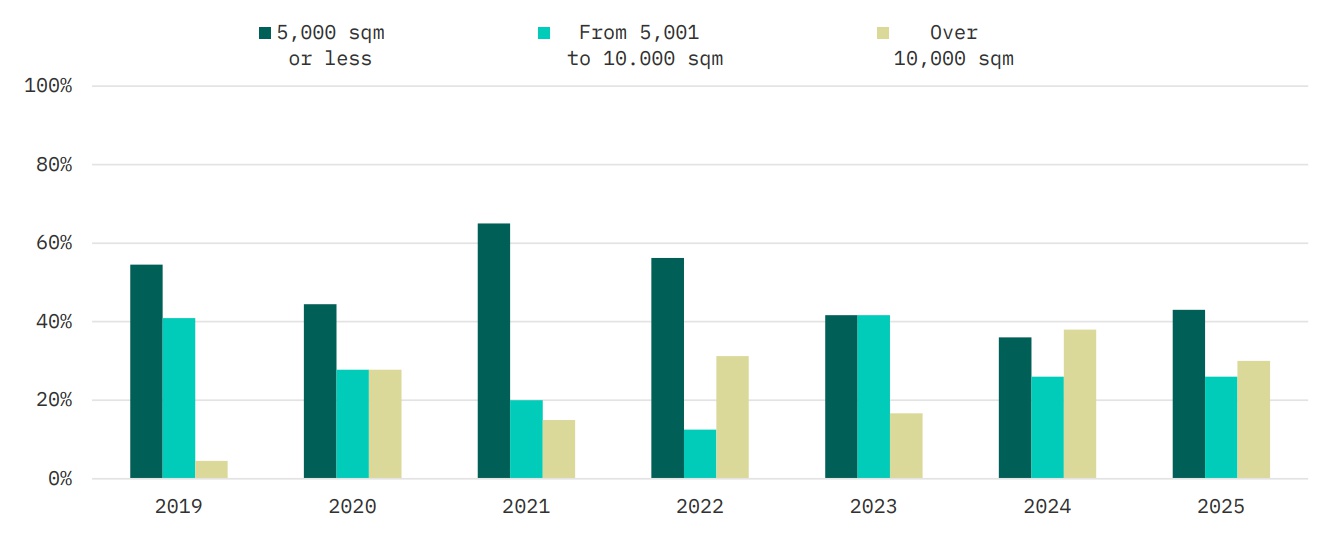

By-Size Leasing Activity, 2025

Despite the challenges associated with the war, 2025 became the most active year for Kyiv’s warehouse real estate market over the past decade. Annual gross take-up amounted to approximately 217,000 sq m (+30% y/y). Demand growth was mainly driven by leasing in newly commissioned warehouse properties, reflecting the realization of pent-up demand for large spaces, as well as tenants replacing warehouse premises damaged since 2022.

Overall, despite the sharp increase in demand, tenant sentiment remained cautiously active. Although relocations (including relocations with expansion) accounted for nearly 70% of leasing activity, this jump in transaction volume came after a prolonged lull in supply and was largely opportunistic in nature. We expect a possible slowdown in activity in the medium term, while business resilience will become the key factor in further leasing decisions.

The wholesale and retail trade segment accounted for 51% of total gross take-up, followed by logistics operators (44%) and pharmaceuticals and healthcare (5%). The e-commerce segment remained the main driver of demand in the sector, as ongoing shifts in consumer behavior and business adaptation to wartime conditions increased reliance on online sales and distribution networks. The pharmaceutical and healthcare sector showed steady growth, supported by the expansion of distributors and pharmacy chains. Throughout 2022–2025, this sector accounted for 10%–15% of annual gross take-up. At the same time, the supply of ready-to-use pharmaceutical warehouses remains limited, prompting tenants to adapt dry warehouses to meet regulatory and technical requirements.

Among the key market transactions were the lease of 40,000 sq m in the Oleksandrivskyi logistics complex by one of the largest national e-commerce operators, as well as a 19,000 sq m deal in the Chaiky logistics complex with an international logistics operator. In addition, leasing activity was further supported by a 14,500 sq m build-to-suit deal under which a leading Ukrainian agro-industrial company is developing a multi-temperature warehouse complex for an international retailer, reinforcing demand for specialized high-quality warehouse properties.

In the deal-size structure, transactions of up to 5,000 sq m accounted for 41% of the total number of deals, but only 10% of the total transaction volume. The share of mid-sized deals (5,000–10,000 sq m) amounted to 23% and 18% of total take-up volume. Large deals above 10,000 sq m accounted for 36% of the total number of deals and 72% of total demand volume. This indicates stable demand for large-format lots, with major retailers and 3PL operators currently remaining the main tenants in this segment.

Supply of Kyiv Warehouse Real Estate

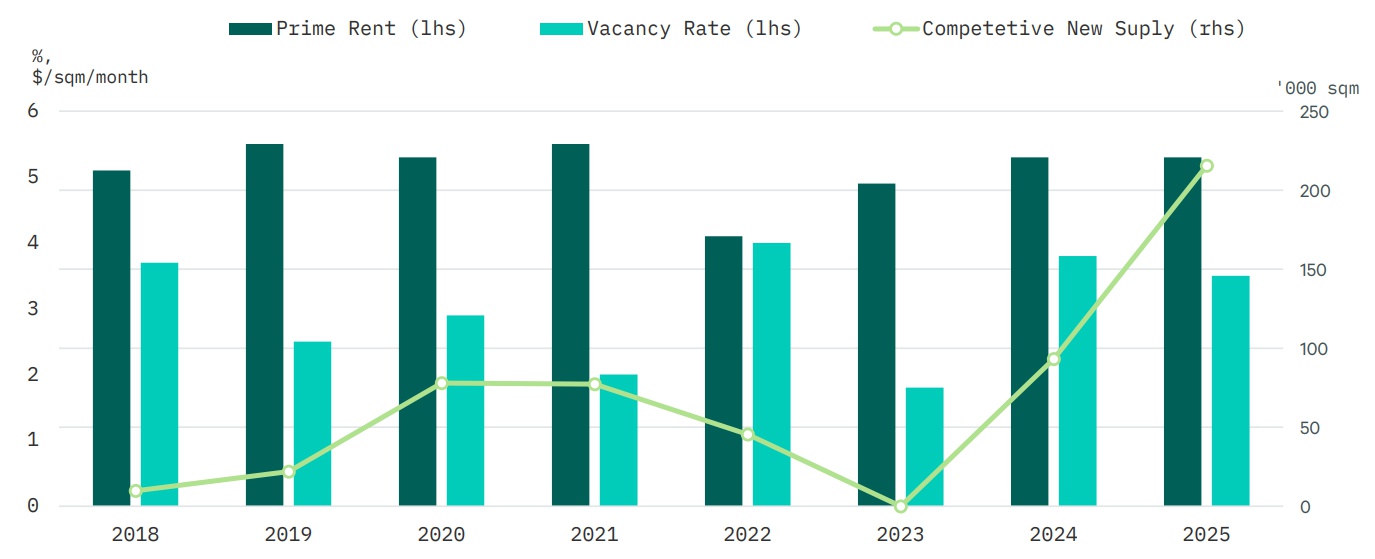

Dynamics of New Supply, Vacancy Rate and Prime Rent, as of H2 2025

2025 became a record year in terms of new completions. The annual volume of new warehouse space amounted to approximately 216,000 sq m, the highest annual supply figure since 2008. As a result, the total volume of competitive supply increased to around 1.57 million sq m (+12% since the beginning of the year), fully recovering to the pre-war level. Among the key new properties were the Oleksandrivskyi logistics complex III–IV (145,000 sq m) and the Chaiky logistics complex IV (32,400 sq m). In addition, 11,000 sq m of warehouse space in the RLC complex, damaged in 2022, was restored and returned to the total competitive supply. Geographically, 78% of new supply was delivered on the left bank of Kyiv, mainly along the Kharkiv highway (M-03). The concentration of new developments in this logistics corridor significantly restored the stock of modern warehouse space that had suffered major damage in 2022.

The volume of future supply for 2026 remains high and is expected to total 90,000 sq m of warehouse space. Among the largest upcoming speculative projects are Chaiky Logistics Complex V (57,000 sq m) and JOULe Warehouse Complex II–III (10,400 sq m). Additional development activity will be generated by built-to-suit projects. In particular, a major national 3PL operator will build two phases of a BTS project with a total area of 26,000 sq m, increasing the supply of new space outside the speculative market.

Vacancy and Rental Rates

Despite the substantial increase in new supply, the vacancy rate declined to 3.5% (-0.3 pp since the beginning of the year). The slight decrease in vacancy occurred even against the backdrop of record development volumes, as most new warehouse properties entered the market with a significant volume of pre-lease agreements, while the remaining space was absorbed shortly after commissioning. As a result, the availability of modern large-scale warehouse space remains limited.

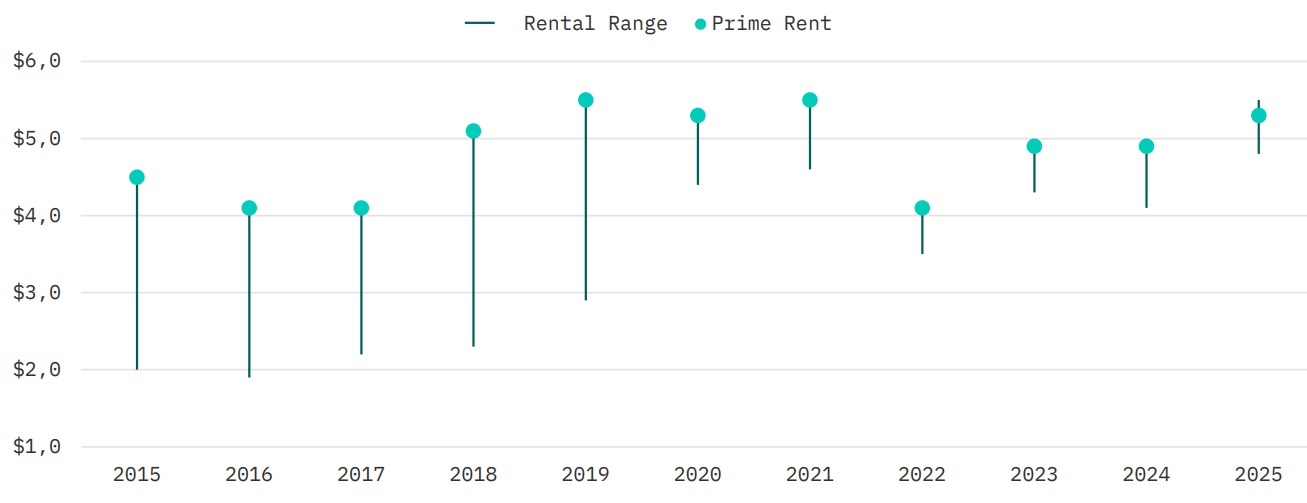

Dynamics of Asking Rental Range and Effective Rent

Quoted rental rates in hryvnia terms for dry warehouses showed an average increase of 9% since the beginning of the year, ranging from UAH 200–250/sq m/month ($4.8–$5.5). The prime effective rental rate remained stable at $5.3/sq m/month (excluding VAT and OPEX), corresponding to the pre-war peak period of 2019–2021. Most lease transactions continued to be concluded in the national currency, reflecting the current macroeconomic environment and exchange-rate volatility.

Quoted rental rates for cold storage warehouses averaged UAH 390–440/sq m/month ($8.5–$10.5), while the prime effective rate remained stable at $9.1/sq m/month. The dynamics of rental rates in 2025 indicate the formation of a more balanced market environment, where rental levels increasingly depend on the quality of the property and its operating characteristics.

Outlook for Kyiv’s Warehouse Real Estate Market

The warehouse real estate market is expected to move into a more balanced phase in 2026 after the record development volumes and leasing activity recorded in 2025. Demand from key tenant groups is likely to remain resilient. At the same time, supply growth will slow, as the volume of future competitive supply in 2026 is projected at 90,000 sq m, which is 58% lower than in 2025.

The vacancy rate is expected to remain low, with a slight upward correction if the projected volume of new supply enters the market. At the same time, vacancy, even with possible growth, is expected to remain within a healthy range. Rental rates are likely to remain stable, supported by the continued absorption of new space, while high-quality warehouse properties will retain stronger pricing attractiveness.

Future Warehouse Supply, 2026

| Name | Developer | GBA, sq m | Direction | Status |

|---|---|---|---|---|

| Chaiky Logistics Complex V | Local | 57,000 | Zhytomyr M-06 | Under construction |

| LOGISTICS niv | Local | 12,000 | Zhytomyr M-06 | Under construction |

| Yantarna, 6 Warehouse Complex | Local | 9,000 | Kyiv | Under construction |

| JOULe Logistics Center (Phase II) | Local | 9,000 | Zhytomyr M-06 | Under construction |

| JOULe Logistics Center (Phase III) | Local | 2,000 | Zhytomyr M-06 | Under construction |

We expect Kyiv’s warehouse real estate market to remain stable in 2026, supported by resilient demand, a gradual strengthening of prime rental rates, and the continued absorption of new warehouse space.

Limited supply of high-quality warehouse space and the gradual strengthening of rental rates create the preconditions for further implementation of build-to-suit projects, particularly for major retailers and logistics operators requiring tailored solutions. In addition, developers are increasingly focusing on undersupplied formats, particularly multi-temperature warehouses, where demand continues to exceed available supply. At the same time, elevated security risks and macroeconomic uncertainty will continue to affect decision-making in the short term.